Ever wondered whether to invest all your money at once or to do that in bits?

Well, if you settled for the latter, you are already practicing the DCA strategy!

Dollar-Cost Averaging (DCA) is an investment strategy where an investor splits the total investment funds to invest in bits.

That is, the investor does not put in the whole capital at once.

But is it actually better than putting in the lump sum at once?

You will find the answer to this and more as you continue on in this post.

Good to go? So am I! Let’s hit the road at once.

DCA Post Outline

To clearly provide all the info you need to know about DCA, here are the subheadings under which I will discuss it:

- What Is Dollar-Cost Averaging?

- How To Calculate Dollar Cost Averaging

- Dollar-Cost Averaging Crypto Platforms

- DCA vs Lump Sum Strategy: Which is Better?

- Conclusion

For details of any of the subheadings, just click on it.

Okay… Let’s begin in earnest now.

What Is Dollar-Cost Averaging?

Dollar-Cost Averaging (DCA) is an investment strategy in which investors divide the total amount to be invested.

With these chunked-up funds, they purchase the target asset at regular intervals, e.g. weekly, monthly, etc.

Once the funds are set, the purchases are made irrespective of the price and at the specified intervals.

For example, John wishes to invest 600,000NGN in Bitcoin for 12 months.

Instead of investing 600k once, he decides to invest 50,000NGN each month.

So, on the first of every month, he buys Bitcoin worth 50,000NGN to hodl.

The whole idea is geared towards reducing the impact of volatility on the overall purchase.

Again, it saves you the stress of constantly checking the market to know the right investment time.

This strategy works best for volatile markets, e.g., cryptocurrency.

Though the number of assets one can buy with fixed funds varies, DCA helps the investor to checkmate losses.

For example, in the example I cited above, Assume John puts in the whole 600,000NGN when the price of Bitcoin is at $26,000, and BTC decides to dip to, say, $17,500.

The loss incurred will be more than when John has invested just 50,000NGN.

This makes it just ideal for newbies in the investment world.

There is no known information on who invented the strategy or how the strategy came to be.

But judging from the available information, this strategy has been in use for a long time (even by people who don’t know it by this name).

In the next subheading, I will use a typical DCA investment to explain how to calculate this strategy.

Scroll down.

How To Calculate Dollar-Cost Averaging

The 15+mins video above contains detailed information on how to calculate your DCA.

But if you prefer to read about it, I’ve got you covered, too! I explained how to do that below.

It’s your choice!

I am going to continue with the example I gave above about John, who wants to invest 600,000NGN.

Assuming John invested his funds, spreading it through 12 months. This is what his calculation will look like:

| Months | Price of BTC (in NGN) | Monthly Investment | Amount of BTC Bought |

| January | 479,950 | 50,000 | 0.0141775 |

| February | 491,100 | 50,000 | 0.1018123 |

| March | 537,000 | 50,000 | 0.0931099 |

| April | 423,752 | 50,000 | 0.1179935 |

| May | 564,900 | 50,000 | 0.0885112 |

| June | 940,000 | 50,000 | 0.0531915 |

| July | 917, 706 | 50,000 | 0.0544837 |

| August | 1,135,000 | 50,000 | 0.0444053 |

| September | 1,640,440 | 50,000 | 0.0304796 |

| October | 1,518,499 | 50,000 | 0.0329273 |

| November | 2,706,222 | 50,000 | 0.0184759 |

| December | 4,035,224 | 50,000 | 0.0123909 |

| Total | 600,000 | 0.5822985 |

The table above explains how John’s investment for a year went.

Assuming John sells off his BTC on the 31st of December at 1 BTC = 5,554,000NGN.

He will get 5,554,000 x 0.5822985 = 3,234,085.87NGN.

To get the profit, 3,234,085.87NGN(Amount after selling) – 600,000NGN(Total investment) = 2,634,085.87NGN

So John made 2,634,085.87NGN as profit from his one-year DCA investment.

Impressive, right?

John might decide to extend his investment period to about 2 years. This means that he will repeat this process (though the price of BTC may vary).

This is how you calculate your DCA investment to know how much profit you have accrued.

The calculation is the same, not minding the type of asset you are investing in.

I must remind you that the performance of your DCA investment depends greatly on the price movement of the asset you are investing in.

Let’s continue to the next section to see crypto platforms that allow you to use this strategy.

Dollar-Cost Averaging Crypto Platforms

DCA is just a trading strategy that can minimise risks and be used in any industry.

However, our interest is in cryptocurrencies. Hence, the platforms I will be listing here allow you to DCA using cryptos.

You can DCA on any crypto platform quite well, but on some of them, you earn more for using them.

Those are the ones I will be listing here and they include:

i. Luno

Luno (formerly Bitx) is a renowned crypto exchange founded in 2013.

It has a Savings Wallet where users can save up their coins and earn interest.

The coins available for saving in the Savings Wallet include:

- Bitcoin: Up to 4% interest per annum

- Ethereum: Up to 4% per annum

- USDC: Up to 7.6% per annum

How this works is that you will create a Savings Wallet for the coin you want to save.

Then, transfer the coin from the exchange’s wallet to the Savings Wallet at no charge.

When you transfer the coin to your Savings Wallet, it is lent to Luno’s trusted partner.

Though the Luno Savings Wallet is meant for long-term investment, you can transfer your coin anytime and at no charge.

*Transfer out…..at no charge here refers to you sending it back to the exchange’s wallet, NOT sending it to an external wallet(that will incur the transaction charges).

NOTE: The interest rate varies with the market conditions and is paid on the 1st of every month.

Find out more info on this here.

ii. Binance

Binance, coined from Binary and Finance, is the biggest crypto trading platform in terms of liquidity.

The Binance Earn feature allows users to increase their crypto holdings.

The main categories of Binance Earn include:

a. Flexible Savings

Here, you can just transfer your coins from the Spot wallet and start earning rewards on them.

The rewards can be redeemed at any time(hence called Flexible).

Interest payment is calculated from the day after your subscription.

The available coins and their Annual Percentage Yield (APY) include:

- BTC: 1.2%

- BUSD: 6%

- USDT: 6%

- 1INCH: 3.29%

- ADA: 1.45%

b. Fixed Savings

Here, you get better rewards but less flexibility. This is because you must set a predetermined duration for your funds to accrue interest.

The duration can be from 7 – 90 days, and the supported coins with their estimated APY are:

- BUSD: 6.31% – 7%

- USDT: 6.31% – 7%

c. Locked Staking

Here, you can earn staking rewards by holding Proof of Stake coins.

You can earn higher rewards if you submit them to be locked for 7 – 90 days.

The available coins here and their estimated APY include:

- USDT: 6.31% – 7%

- BUSD: 6.31% – 7%

- USDC: 5.31% – 6%

d. Liquid Swap

To do this, you can become a market maker by depositing one or more supported assets and starting to earn interest.

The supported assets include BNB, BUSD, WBTC, BTC, ETH, DAI, USDT, AUD, USDC, GBP, and EUR.

Your total rate of return is calculated based on the interest paid the previous day, liquidity rewards, and all trading fees.

You will get no return rate on liquidity rewards at the start of the activity.

e. BNB Vault

Here, you will stake your BNB and receive your BNB vault assets.

The reward will start counting from the second day and is sent daily.

Just like in Flexible Savings, you can redeem your funds anytime.

There are also others, such as Lending Activities, Launchpool, Dual Savings, etc.

iii. Kucoin

This platform is a crypto trading platform that allows its users to save using the DCA strategy.

Its DCA works with the Trading Bot and is only available on its mobile app.

The coins available for DCA on Kucoin include:

To invest in any of these coins, you have to make a payment with USDT.

How this works is that you will click on the Trading Bot to create one.

Then, you will select the coin you want to save and set the amount (minimum is 10 USD) and time for the investment.

You will then be required to adjust and set your profit target.

The bot will then calculate the time it will take for your profit target to be reached based on historical data.

You can also opt for the bot to:

- Remind you and continue trading when the target is reached

- Remind you and sell all positions once the target is reached

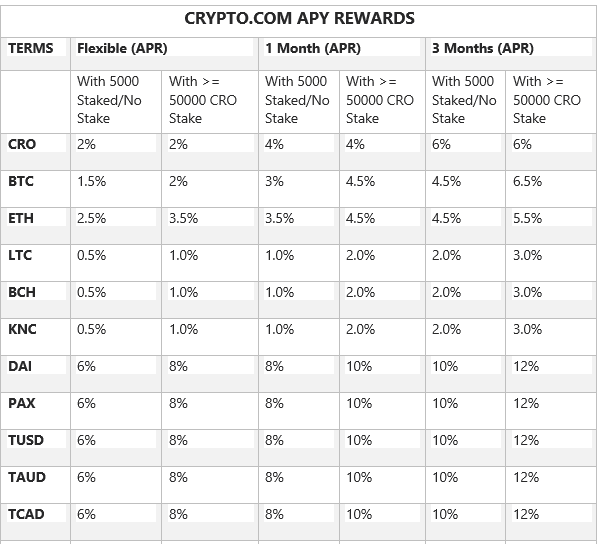

iv. Crypto.com

Crypto.com is a crypto trading platform that was founded in 2017.

It is headquartered in Hong Kong and has a Crypto Earn feature where users earn rewards for staking their coins.

You can choose between Flexible, one–month, and three–month investments.

Thus, the interest you will receive depends on the type of investment you wish to embark on.

The table below shows information on the supported coins and their estimated value.

Read more: Crypto.com Review: All You Need To Know

You can also DCA with some of the wallets that pay high interest, e.g. Exodus, Atomic Wallet, Trust Wallet, etc.

You can invest in any coins by buying them and then transferring them to your chosen wallet.

However, be sure to always send enough to settle the transaction fees.

So here you have the platforms to carry out your savings using the DCA strategy.

Next, I will compare the Lump Sum investment strategy to DCA to find out which is better.

Keep reading.

DCA vs. Lump Sum Investment Strategy: Which Is Better?

Lump Sum investment is simply an investment strategy in which the investor invests all the funds at once.

This is unlike what we have in DCA, where the investor has to split the money in bits and invest each bit at a specified time.

For starters, both strategies are good. It all depends on the investor’s choice and the market conditions.

I will explain further what I mean by bringing back the example of John I used above.

Bullish Year Calculation

The table below is what John made via DCA in the year 2017.

| Months | Price of BTC (in NGN) | Monthly Investment | Amount of BTC Bought |

| January | 479,950 | 50,000 | 0.0141775 |

| February | 491,100 | 50,000 | 0.1018123 |

| March | 537,000 | 50,000 | 0.0931099 |

| April | 423,752 | 50,000 | 0.1179935 |

| May | 564,900 | 50,000 | 0.0885112 |

| June | 940,000 | 50,000 | 0.0531915 |

| July | 917, 706 | 50,000 | 0.0544837 |

| August | 1,135,000 | 50,000 | 0.0444053 |

| September | 1,640,440 | 50,000 | 0.0304796 |

| October | 1,518,499 | 50,000 | 0.0329273 |

| November | 2,706,222 | 50,000 | 0.0184759 |

| December | 4,035,224 | 50,000 | 0.0123909 |

| Total | 600,000 | 0.5822985 | |

| Sell off @ 31st Dec. 2017 | @ 1BTC = 5,554,000NGN | 3,234,085.87 | Profit: 2,634,085.87NGN |

So John made 2,634,085.87NGN as profit from his one-year DCA investment.

Let’s look at this same investment with the Lump Sum Strategy.

John purchased the coins and hodl until December 2017 and then sold them. This table provides a breakdown of how his investment went.

| Investment period | January 2017 |

| BTC Price @ January 2017 | 479,950 NGN |

| Investment Capital | 600,000 NGN |

| Amount of BTC bought | 1.2501302 BTC |

| Sell off Period | December 2017 |

| BTC Price @ December 2017 | 5,554,000 NGN |

| 1.2501302 x 5,554,000 = 6,943,223.13, | |

| Profit (Sell-off price – Investment capital) | 6,943,223.13 – 600,000 = 6,343,223.13 |

Looking at the above instances, you will see that John made a profit in both cases.

However, the profit made when using the Lump Sum Strategy is bigger than when the DCA was used.

This is because(for the Lump Sum) John invested all the funds while the price of BTC was low. Over the subsequent months, the price of BTC increased.

Hence, the very high profit.

For the DCA, John kept buying even as the price of BTC increased. Thus, leading to a smaller profit.

But as I pointed out earlier, this is because of the market condition (it was bullish).

Assuming it was a bearish market, the loss’s impact on DCA will be less than that of the Lump Sum strategy.

Let’s see the illustration below for a bearish year (2018).

Bearish Year Calculation

| Months | Price of BTC (in NGN) | Monthly Investment (in NGN) | Amount of BTC Bought |

| January | 5,410,410 | 50,000 | 0.0092414 |

| February | 3,068,236 | 50,000 | 0.0162960 |

| March | 4,037,059 | 50,000 | 0.0123853 |

| April | 2,431,000 | 50,000 | 0.0205677 |

| May | 3,498,001 | 50,000 | 0.0142939 |

| June | 2,790,699 | 50,000 | 0.0179167 |

| July | 2,221,001 | 50,000 | 0.0225124 |

| August | 2,481,129 | 50,000 | 0.0201521 |

| September | 2,569,912 | 50,000 | 0.0194559 |

| October | 2,313.994 | 50,000 | 0.0216077 |

| November | 2,278,000 | 50,000 | 0.0219491 |

| December | 1,519,983 | 50,000 | 0.0328951 |

| Total | 600,000 | 0.2292733 |

The price of BTC on 31st December 2018 is 1,389,989 NGN.

So if John sells off at that point, he will have 1,389,989 x 0.2292733 = 318,687 NGN.

So, from his investment capital, John lost (600,000 – 318,687) = 281,313 NGN.

Let’s see how it went with a Lump Sum investment:

| Investment period | January 2018 |

| BTC Price @ January 2018 | 5,410,410 NGN |

| Investment Capital | 600,000 NGN |

| Amount of BTC bought | 0.1108973 BTC |

| Sell off Period | December 2018 |

| BTC Price @ December 2017 | 1,389,989 NGN |

| 0.1108973 x1,389,989 = 165,371 NGN | |

| Loss (Sell-off price – Investment capital) | 165,371 – 600,000 = -434,629 NGN |

I guess by now, you would have gotten the gist.

There were losses in both methods, but the one of the Lump Sum Strategy is more. The loss was almost double what you have for DCA!

So, in answering the question of which strategy is better, this is my verdict:

Though both strategies are very good, and the market condition plays a vital role in the outcome of both cases, I prefer DCA.

This is because it is the go-to strategy for newbies and even some market veterans concerned with minimizing risks.

Again, our human psychology prefers making gains to making even a single loss.

Thirdly, not everyone has the lump sum to invest all at once.

So investing a set amount of funds at a specified time is the only way most persons can invest to ensure losses are controlled.

DCA’s ability to minimize the risk of loss greatly endears it to investors.

DCA’s only fault is that the investor might miss out on higher returns, and it is not a certified solution to all other investment risks.

However, some investors will still choose the Lump Sum Strategy based on the conventional belief that prices will keep rising.

And when such happens, Lump Strategy investors cash out really big.

So, in the end, I think it all boils down to the investor’s choice.

Please note that this is in no way investment advice. Do your due diligence before embarking on any investment spree.

Okay, enough of the writing!

Let’s go and wrap this discussion up in the next section.

Conclusion

This is the last part of our discussion, where you give me feedback on what we’ve discussed so far.

Talk about saving the best for the last!

So far, I have guided you through the DCA strategy, explained how to calculate it, and compared it with the Lump Sum strategy.

I know you picked a thing or two you want to discuss. But before we get to you, tell me:

Do you use the Dollar Cost Averaging strategy? How has it been thus far?

If you are yet to start up, which platforms will you use? Why?

Do you have any questions to ask me?

Go now to the comment box below to air your views and ask any question(s) you might have.

Remember to give this post a share (oops…I just did!).

Click on the social media buttons right below to share.

")

You are welcome.

I’m glad you enjoyed it.

I’m loving this DCA idea…THANKS Amaka for making it super clear